Follow Yesler for the latest on the LBM industry

PART I

WILL LUMBER PRICES ACHIEVE A “NEW NORMAL?”

Record lumber prices have led some traders to suggest a “new normal” pricing floor exists in the lumber market. Their hypothesis is that a combination of producer leverage and discipline would permanently buoy prices above prior lows. That’s just not how lumber markets work. While there may be temporary floors, intracycle stability or bounces, the floor will remain unchanged and equal the cash cost of the inputs to lumber production.

In part one of this two-part series, we’ll explore the commodity cycle and demand to supply ratios that influence price.

Two cycles, one commodity

Lumber is a commodity. Number 2 Southern Yellow Pine (#2 SYP) you buy from producer A, meets the same performance requirements as the #2 SYP from producer B. They don’t always meet the same perception of quality to buyers (mold-free, tight knots, four square edges, etc.), but neither the architect, engineer, nor building inspector care. #2 SYP is interchangeable, and the same interchangeability exists within other species and even between species to a large extent.

Perceived quality can help manufacturers capture marginally higher prices or “last-look” from buyers. A manufacturer’s reliability – on-time shipping, lead-time commitments, and overall production quality and consistency – can also create marginal price advantage. But interchangeability by grade and species means price wins as the market mechanism to clear imbalances in supply and demand.

There are two cycles that govern the price of commodity lumber.

First, is the long-term cycle, governed by long-term supply and demand imbalances. Consider the Great Recession when housing starts retreated from 2.2 million to less than 600k. This created a dramatic imbalance between supply (excess) and demand. Lumber prices fell to rock bottom.

Second, is the short-term cycle. A rail strike in Canada, for example, creates a temporary imbalance of supply and demand based on rail shipping capacity out of British Columbia. Forest fires that temporarily halt log harvesting in Oregon also create a temporary, regional imbalance. Both can send price ripples across the entire US. Neither of these change the long-term balance, but they do constrict supply and create upward price pressure.

The COVID shock was a similar short-term cycle, with some mid-term reverberations. We have yet to see if COVID fundamentally altered the underlying demand in the housing market, but for now, the housing market continues to operate within the historic norms of demand (1.3-1.5 million annual starts). Long term commodity cycles and the resulting prices are influenced by macro demand (global and national trends) and macro supply (investment strategies and capital markets). The primary supply side variable is North American lumber production. One big demand side variable is US residential housing starts.

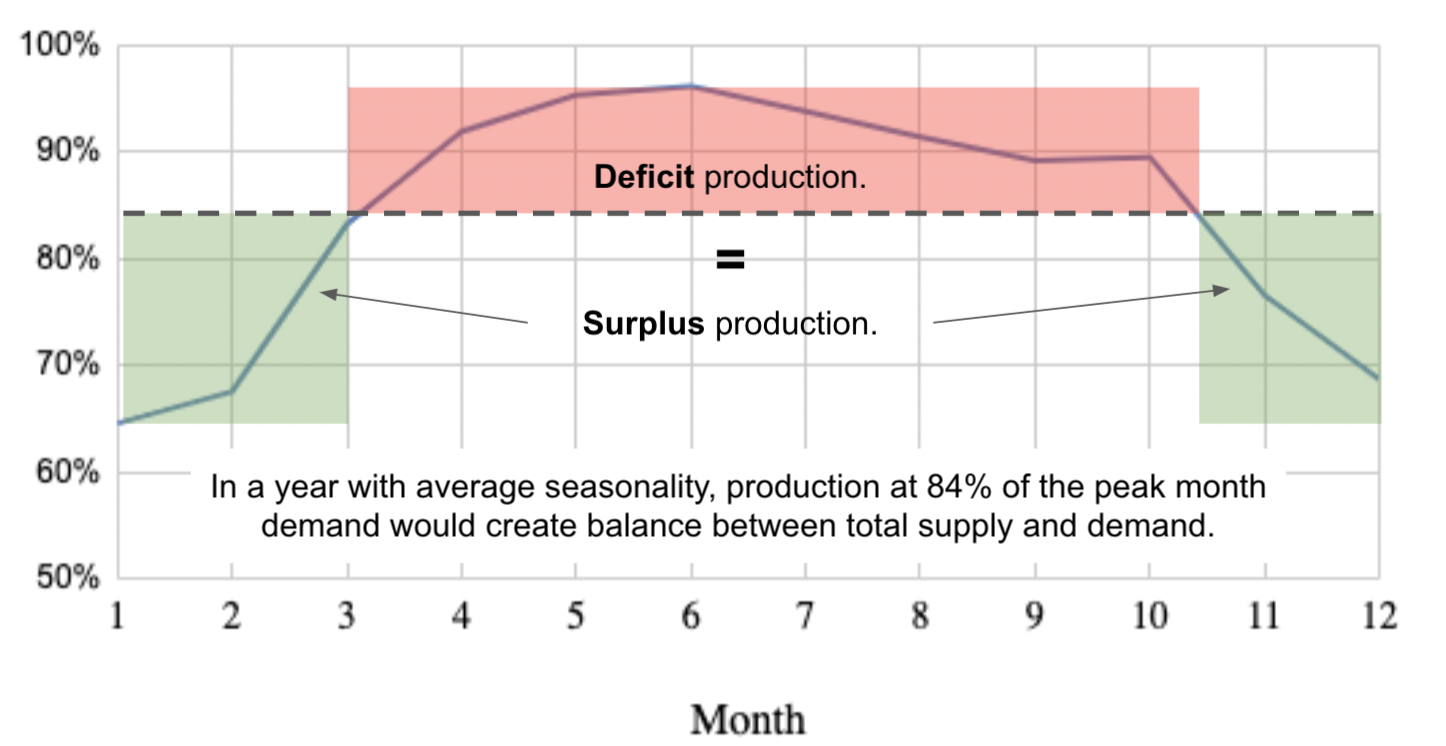

Demand and Supply are in balance when production is 84% of peak annual demand

There is a ratio of demand to capacity, below which pricing will achieve rock bottom, like it did post Great Recession, and above which pricing will run hot like the first half of 2021. It’s difficult to calculate the ratio because it can be hard to determine the actual productive capacity relative to demand in any given month. But understanding the threshold ratio is easy, because its basis is the seasonality of average demand – it’s 84%.

When sustained demand for lumber (monthly housing starts as a proxy for demand) exceeds 84% of the productive capacity to supply the lumber, then there is upward pressure on price. When sustained demand remains below 84% of the productive capacity, there is downward pressure on price. How low can the price go? All the way down to the cash cost of lumber. The old normal.

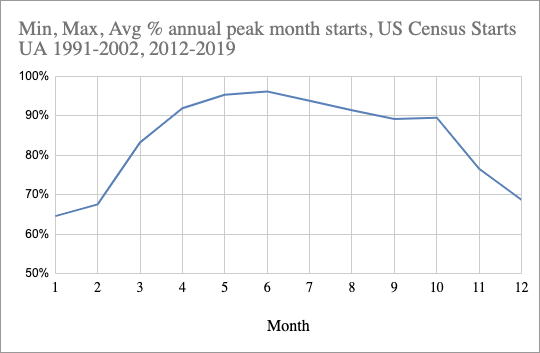

This 84% rule of thumb is derived straight from US Census Housing Starts. Ignore seasonally adjusted numbers and instead look at actual monthly start numbers. The graph below shows that average monthly housing starts fluctuate from a low of 64% of peak-month starts (actual monthly starts as a percentage of the peak month within each year) to 96% of peak-month starts from 1991-2002 and 2012-2019. I chose these years because they include only stable, steadily rising markets like we are in right now. The average of all monthly percent of peak demand is 84%.

By month, % of peak annual housing starts, US Census, 1991-2002 and 2012-2019

Why 84%? Consider this: If mills operate at a capacity that perfectly matches 84% of the peak demand for the year, then the extra inventory they produce in the winter (green shading in the chart below) fills the deficit of underproduction in the summer (red shading in the chart below).

Why isn’t the peak month 100% and wouldn’t this make the average higher?

In any given month, June for example, there are 27 years of data represented above. Some of these June data are the actual peak month, 100%, the highest month in the year. Sometimes the peak occurs in July, May, or even October, reducing June from 100% to something lower, maybe even 92%. As a result, the average % of peak for June is 96%.

Similarly, the average % of peak for the winter months is a range, with the low of 64% as an average of 27 data points for each month. The range of numbers is much more broad in the winter (bad weather) and the range more narrow in the summer (good weather). Using all that data, the low is 64%, the high is 96%, and the average is 84%. The graphs show the average of each month for 27 years, instead of all 27 years in one chart. Using monthly data normalized to the peak within the year puts all data on the same scale from 0-100%.

In a perfectly balanced market, pricing power shifts to sellers in the summer and buyers in the winter, with the timing of purchases and inventory positions altering elasticity of price and amplifying volatility. Any sustained period of greater demand drives prices higher. This enables marginal overtime production or additional or longer shifts at mills to capture profit, and improves the economics for importers of global supply (Europe). Any sustained period of lesser demand drives prices lower as suppliers compete to move volume out of their mills.

Over a longer cycle where demand exceeds supply, companies invest in new production capacity. This increases capacity relative to demand. When long cycle demand declines (like during the Great Recession), the industry is left with excess production. Suppliers must play a dangerous game, tapping their cash reserves until one operator shuts down their production to reduce supply and shifts the balance of demand to supply for the remaining producers. The price then bounces back above cash cost as demand and supply find balance.

The cyclical nature of the lumber market is at odds with traders’ desire for influence and control, and also ego. Favorable outcomes, like rapidly rising profits, are commonly claimed as professional prowess, while unfavorable outcomes are disclaimed and attributed to the market. In the end, supply and demand drive prices. Good buyers and sellers compete for marginal advantage on a price dynamic out of their immediate control.

In the next segment we’ll explore the limited influence individual buyers and sellers have on market prices leading to the conclusion that there is no new normal for price. The cash cost of production will remain the pricing floor.